Compliance Update – June 2018

25th June 2018Welcome to our compliance update. In this edition we describe:

- the trend towards participation rather than performance based payments for ideas

- the up-tick in firms joining TIM

- a note of caution on the compliance aspects of alternative data

- the increased usage of TIM’s Restricted List compliance feature and how it helps protect sell sides and buy sides in their trade idea communications.

Trade idea payment mechanisms

Historically systematic firms have rewarded trade ideas based on performance. Post-MiFID II, new systematic firms that have launched trade ideas programs have been using a “pay-for-participation” model.

Until 2017 reward mechanisms for trade ideas were skewed towards top performers, with the the top 30-50% of participants receiving most or all of the rewards. The rewards often came in the form of additional flow for brokers with which the buy-side had trading relationships, and CSA payments for brokers that the buy-side did not trade with. Sales people at brokers were normally happy with this principle on the optimistic premise they would outperform the average. However, this could lead to awkward conversations with participants that just missed out.

A majority of our recent buy-side launches have opted for a “pay-for-participation” model. Under this model the contributor is paid provided that a minimum number of ideas in the measurement period is met. The rise in popularity of the pay for participation model, with their more certain payment flow, may be prompted in part by compliance concerns. While long-term consumers of trade ideas may feel comfortable that it is within the spirit of MiFID II unbundling to pay only contributors that perform well, new participants may feel the need to pay all contributors quarterly – even those that don’t perform – to meet MiFID II requirements for paying for research. Similar concerns can restrict trial periods for live ideas to 3 months or less.

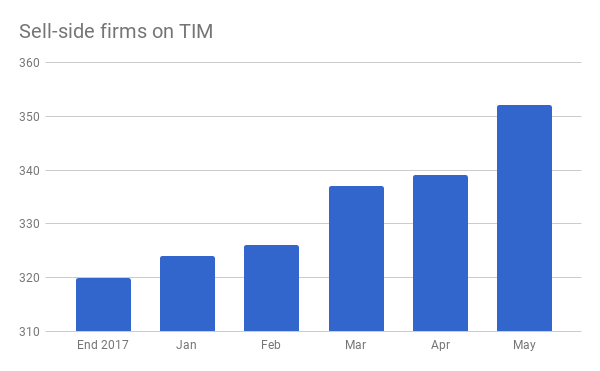

Perhaps not surprisingly, smaller firms and independent research providers have responded most positively to the pay for participation model. TIM has seen an upsurge in firms joining the service (Fig. 1) to take advantage of the more certain rewards on offer.

Rise of the IRPs

Some of the smallest firms on TIM are independent research providers (IRPs), a community that is starting to take to ideas. Certainly Sequoia thinks that there is a positive environment for IRPs. Sequoia has led an investment round putting $21 million into newcomer Smartkarma, a Singapore-based technology provider that enables IRPs to enter and distribute their insights. Smartkarma aims to provide a full service for IRPs, up to and including office space for those that need it. This is good news for analysts that may lose their jobs at large brokers – a worry if JP Morgan’s estimate is correct that research payments have fallen 25% so far this year, with another 25% fall to come.

Rise of alternative data

The rise in interest in alternative data sets is well documented. TIM is exploring existing and new data sets, and we have established a working group to determine where we can add most value. We’re learning that each new data set brings its own possible compliance issues. For example the next big data set may be geolocation data. But at least one expert – Leigh Drogen, CEO of Estimize – advises that the compliance hurdles for this data are unlikely to be overcome in the next couple of years.

We’re also finding that our experience in trade ideas is highly relevant to new data sets. We’ve developed relatively unusual skills in compliance, aggregation, conforming, performance measurement and distribution of data sets. For example, our ability to conform data is something our quant clients appreciate. When we look at a historic data set, we analyse the data for anomalies, looking at returns distributions to ensure the data has not been tampered with, multiple history files and real time data to ensure consistency, and add open and licenced ticker codes relevant to the time the data was available.

TIM Restricted List feature helps reduce risk

Increasing numbers of sell-sides are implementing their Restricted Lists in TIM. The restricted lists implementation is reassuring for both idea contributors and buy-side recipients because it minimises the risk of inadvertently giving insider information. If you are not familiar with the feature, TIM can either provide a warning when a salesperson enters an idea on a stock on the restricted list, or block it altogether. Salespeople are also notified when an existing idea is on a stock is added to the restricted list, enabling them to take the appropriate action. For more information, contact us on compliance@timgroup.com.